It is wiser and safer to be prepared for any future rather than trying to predict a particular one.

The most important thing (after your behavior)

In the long term, more than 90% of any portfolio’s return depends on its asset allocation policy, not the individual fund/stock selection. Choosing the most appropriate asset allocation model —consistent with the nature of the markets— is the key piece when building a profitable investment strategy.

Therefore, it is useless to waste time and energy looking for the best hedge fund or the next stock bagger. We must find an asset allocation model that is not in contradiction with the way markets are.

The Ugly Truth about the Markets

Real knowledge is to know the extent of one’s ignorance.

―Confucius

So what is its nature? That markets are unpredictable.

Empirical evidence strongly shows that the ability to predict the future evolution of emerging social phenomena —like politics, economics or financial markets— is nonexistent and not persistent (see here, here, here and here).

Even when some guru or “expert” —among the thousands of forecasters out there making new predictions every day— hit the last turn of the market, we cannot know if he was lucky —and we know it will not persist. In other words, it is useless to seek and follow those who have succeeded in anticipating recent market developments, as their past success does not imply that they are able to continue in doing so.

Why Markets are unpredictable?

Notice that the unpredictability of the markets is not because we are not intelligent enough, we lack information, or we do not have enough technological means: The impossibility of predicting the markets is an epistemological consequence of their intrinsic nature as a by-product of human action (more → here).

What can we do?

The unpredictability of markets has two fundamental consequences when investing. The first is that risk management must be convex.

The second is that if it is not possible to forecast consistently whether one economic scenario is more likely to occur than another in the following months, we cannot justify allocating more weight to one asset over another in the portfolio. Therefore the only asset allocation model, rational and coherent with our inability to predict the future, is an equally-weighted portfolio.

Indeed, empirical evidence shows that the most robust asset allocation model, with the best ex-post results, is the equally-weighted or Portfolio 1/N (DeMiguel et al 2009), beating in the long term more popular and sophisticated techniques as Markowitz optimization, Black-Litterman, Risk-Parity, etc.

Keeping things simple is the best strategy in complex and unpredictable environments such as financial markets (more here). That’s why the Austrian Strategy implements an equally weighted portfolio covering all states of the economic cycle with a global exposure.

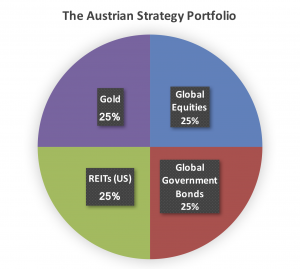

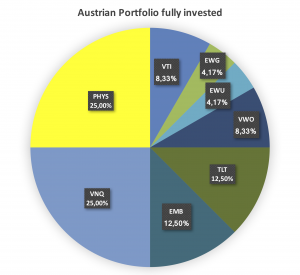

Building an Equally-weighted Austrian Global Portfolio

It is important to realize that moving from an abstract idea to its actual implementation implies making inevitable concessions. Indeed, the financial instruments available and the practical limitations of the real financial world will condition what we can achieve in practice. Thus, this proposed implementation of the Austrian Strategy is the best I have found yet, built with ETFs (it is possible to implement it in a more profitable way using Futures instead of ETFs, but then a larger volume of investment is necessary), without giving up to continuously improving the current implementation as the industry offers new and better instruments.

Having these limitations in mind, global exposure to each asset class is achieved through ETFs that replicate —in an efficient, liquid and cost-efficient manner—, the main indexes of each asset class around the world. Notice that equally-weighting a portfolio naturally puts a ceiling on the maximum exposure per asset type of 25% (¼ for every global classic asset type of Equities, Long-Term Gov. Bonds, Gold, and REITs).

Global Equities (25% of the portfolio): VTI, EWG, EWU, VWO

Typical world indices —as the MSCI ACWI— have about 60% exposure to USA stocks. This excess of weighting in a single country/region is too far from the principle of equalization derived from the impossibility of predicting the future (we cannot know which country/region will perform best in the future).

To avoid this excess concentration, for the time being, the Equities investment is divided into three equal parts of 8.33% (25%/3) each: US (VTI), Europe and Emerging Markets.

Likewise, in Europe we will limit the exposure to its two main economic powers —Germany (EWG) and the United Kingdom (EWU)—, splitting its 8.33% weight into 4.16% (8.33%/2) each country.

We leave the exposure to Emerging Markets (VWO) through a single index, as it is not necessary at the moment to increase the resolution (splitting into more individual countries) in that region.

Global Government Bonds (25%): TLT, EMB

Ideally, the goal would be to invest in as many (safe) government bonds as we could. But due to operational complications, investment in bonds is limited to the regions of the USA (TLT) and Emerging Markets (EMB), 12.50% (25%/2) each.

REITs (25%): VNQ

Although REITs —as an optimal financial investment vehicle to gain exposure to the real estate market and its properties— have become popular worldwide throughout the last few years, their efficiency outside the USA leaves much to be desired. The long-term growth of REITs outside the USA is not significant enough to justify diversification beyond US borders. For the time being it is limited to the US REITs (VNQ).

Gold (25%): PHYS

There are many ways to get exposure to gold, but PHYS is particularly convenient for US investor because of its tax advantages while providing the same properties and safety as any other regulated top gold ETF.

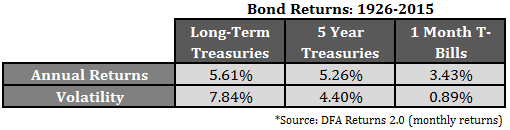

Cash-Equivalent (% variable depending on risk control): IEI

Short-term bonds (from 1-month T-Bills to 1-year Treasuries) are usually used as liquidity equivalent and safe haven. But there is no significative increase in risk if instead of short-term bonds we use 5-year Treasuries in the Austrian Portfolio.

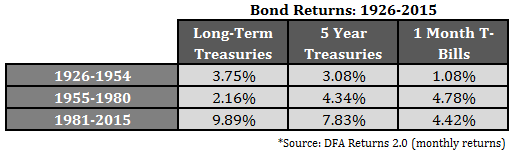

On the contrary, its great stability across any economic environment (even when interest rates rise as during 1955-1980) hardly adds volatility to the portfolio and improves its returns on the medium and long-term.

The Austrian Portfolio fully invested (with no risk control):

This Austrian Strategy portfolio answers the first two questions on investing (What assets to invest? and What asset allocation model?), from an Austrian Economics point of view as it is:

- Able to capitalize on any state of the global economy and

- Coherent with the impossibility to forecast the future.

To complete the Austrian Investment Strategy, a layer of risk management —also consistent with the nature of the financial markets— needs to be added here.

→ Don’t forget to look at what assets to invest in and what risk control to implement